Credit cards can be a useful tool for building credit and covering unforeseen expenses, but they do require that you use your card wisely. Having a strong credit profile is a crucial decision factor used by landlords, utility companies and other financial institutions. A low credit score or high debt can reflect poorly on an applicant, possibly resulting in denial. Additionally, if credit is managed incorrectly, it can cause significant debt, high interest rates and financial burden.

As a first-time credit card holder, it’s important to learn how to manage your spending, what you should consider before applying and what credit card may be the best option for you.

Should You Get a Credit Card?

Getting your first credit card can be exciting as it increases your buying power and gives you the opportunity to start building your credit. Before you apply for a credit card, be sure you understand how credit cards work and how you plan on using credit. These initial steps can help keep you financially successful and avoid overusing your credit.

Why a Credit Card May Be a Good Option for You

Credit cards provide a variety of benefits to cardholders, including securely purchasing everyday or big-ticket items. If you’re on the fence about whether you should or shouldn’t apply for a credit card, below are a few benefits a credit card offers.

1. INCENTIVES AND REWARDS

There are plenty of credit cards that offer extra incentives or rewards for cardholders, such as cash back, points, shopping and student discounts, frequent flyer miles and some even offer airport lounge access or rewards at partner merchants. These types of rewards can help you save in the long run and provide perks based on your preferences and interests.

2. EASE OF USE AND CONVENIENCE

Most businesses accept credit cards as a form of payment. This means that wherever you are in the world, your credit card is likely to get accepted, especially if it’s from a well-known credit card issuer such as Visa and Mastercard. A credit card also decreases the need to carry cash on you.

3. BUILD YOUR CREDIT

A credit card is one of the most popular ways to build credit. As a responsible credit card user, you can easily build a positive credit score to open up financial opportunities for you. A good rule of thumb to boost your credit is to spend what you can pay off the next month in full, maintain on-time payments and have a zero balance on your card.

4. KEEP YOUR ACCOUNT SECURE

In the unfortunate situation your credit card information is stolen or your online identity is compromised and your credit card is used, you can immediately secure your account by filing a fraudulent purchase claim. You must report the card or card number as stolen as soon as possible and work with your credit card company on reversing the charges. Many credit card companies also offer email or text alerts that will contact you when questionable or large purchases are made. This helps ensure that fraudulent purchases are caught as soon as they’re made and your account can be closed or suspended to stop additional fraudulent expenses.

5. TRACK YOUR SPENDING

You can easily track your credit card spending through your account statement or bank’s online portal or mobile application. By keeping tabs on your spending, you can also ensure you’re staying within your budget and on track to reaching your financial goals. It can also help you course correct if your spending is going over your budgeted limits. Some issuers may even let you generate reports to let you see what categories you spend on the most during a certain period.

Why You Shouldn’t Get a Credit Card

Despite all the benefits a credit card could provide, it’s important to determine if it’s the best choice for your financial circumstances. Getting a credit card may not be the best choice if you’re currently living paycheck-to-paycheck, if you’re a heavy spender, you’re frequently outside of your budget, or if you’re currently working on repaying debt.

There are several factors to help you determine if a credit card is the best option for you outlined below.

1. ACCRUED INTEREST

If you tend to not be able to pay your balance off in full each month, you may want to opt for a debit card or cash instead. Credit card interest fees can reach staggering heights — with the average standing at 17.13% in 2021.

2. TESTS YOUR SPENDING SELF-CONTROL

While having a credit card can help you track your budget, it can also just as easily help you ignore it. It’s easy to forget how small charges can rack up, especially if you’re operating on what is essentially borrowed money. It can also be tempting to use it for large purchases which could lead to long repayment times with accrued interest.

3. LATE PAYMENT PENALTIES

If you aren’t sure you can make the payments, you may be better off foregoing a credit card until you’re in a better place financially. Credit cards can penalize you with additional interest for late payments, sometimes even going as far as charging the maximum interest rate.

4. VARYING FEES

It’s important to read the fine print closely when you get a new credit card. There are plenty of fees connected to your account that you should be aware of, such as your annual fees, annual percentage rate (APR), late payment fees and balance transfer fees. If you don’t familiarize yourself with these potential fees, you may end up with a higher bill than you expected at the end of your billing cycle or see annual fees you may not have budgeted for.

5. IT CAN PUT YOU INTO GREATER DEBT

If you’re already holding some form of debt, whether it’s through loans, unforeseen expenses or continued catching up from a financial hit, getting a credit card could put you into greater debt if you’re not careful. A MoneyGeek study shows that 18% of Americans find managing credit card debt as their greatest source of finance-related stress. If you feel you aren’t in the best place to handle credit card expenses, you may want to hold off on applying for one.

5 Factors to Consider Before Getting Your First Card

There are a number of factors you should consider prior to applying for your first credit card, such as your spending habits, current credit history and what you can financially take on. After all, the right credit card should help you build your credit profile, not make it more difficult for you to increase your score. Below are five factors to consider when applying for your first card.

Your eligibility – There are a range of credit cards available on the market, but keep in mind that not all cards may be available to you as a first-time cardholder. Some cards have prerequisites including high-income earner status, long-time cardholder, or maintain an excellent credit score.

Your eligibility – There are a range of credit cards available on the market, but keep in mind that not all cards may be available to you as a first-time cardholder. Some cards have prerequisites including high-income earner status, long-time cardholder, or maintain an excellent credit score. Your financial capacity – Consider where you financially stand before applying for a credit card. Are you struggling to pay your bills every month? Are you currently paying down debt? If so, you may want to skip getting a credit card until your finances are more stable.

Your financial capacity – Consider where you financially stand before applying for a credit card. Are you struggling to pay your bills every month? Are you currently paying down debt? If so, you may want to skip getting a credit card until your finances are more stable. Your financial habits – Even if your financial situation is good, understanding your financial habits can help you determine if a credit card is right for you. If you are an impulsive shopper or you overspend your monthly budget, you may want to consider sticking to your debit card until you’ve strengthened your financial habits and avoided racking up debt.

Your financial habits – Even if your financial situation is good, understanding your financial habits can help you determine if a credit card is right for you. If you are an impulsive shopper or you overspend your monthly budget, you may want to consider sticking to your debit card until you’ve strengthened your financial habits and avoided racking up debt. Your needs and alternative options – Ask yourself why you need credit. Do you crave the security of having additional funds available for emergencies? Do you want to make a large purchase? Are you seeking a long-term financing option? If you discover that you’re seeking additional financing for large purchases, you may benefit from a loan and a lower interest rate than a credit card.

Your needs and alternative options – Ask yourself why you need credit. Do you crave the security of having additional funds available for emergencies? Do you want to make a large purchase? Are you seeking a long-term financing option? If you discover that you’re seeking additional financing for large purchases, you may benefit from a loan and a lower interest rate than a credit card. Your current credit history – You may be denied an unsecured credit card if you have little-to-no credit history or less-than-perfect credit. You can obtain a free credit report and review it before you apply. This way, you can dispute any errors and increase your chances of getting approved. If you’re interested in improving your credit history, a secured credit card — a credit card that you add money to and use to build credit — may be a good option to help boost your rating.

Your current credit history – You may be denied an unsecured credit card if you have little-to-no credit history or less-than-perfect credit. You can obtain a free credit report and review it before you apply. This way, you can dispute any errors and increase your chances of getting approved. If you’re interested in improving your credit history, a secured credit card — a credit card that you add money to and use to build credit — may be a good option to help boost your rating.

How to Pick the Best First Credit Card

With the vast number of credit card options on the market, choosing the best card for your needs is important. Selecting a card with the right balance of fees and rewards can help ensure you use it for the right reasons and avoid going over your budget.

Whether you’re a student or a young adult getting your first card, to understand how to choose the best credit card, it’s important to learn the different types of cards available.

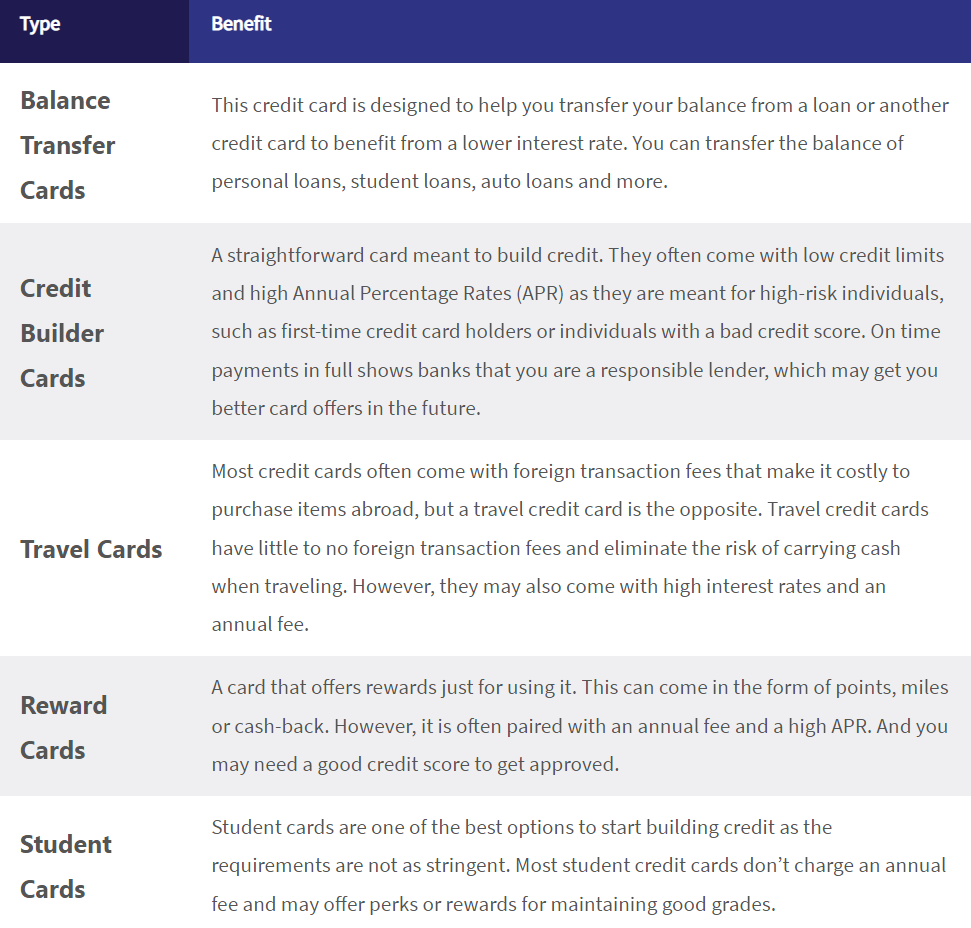

Credit Card Types

There are a variety of credit cards available on the market that can make the choice difficult, especially for first-time cardholders. Each card type has its own pros and cons that meet different needs, which is why it’s important to identify why you need the credit card in the first place. Learn about the different types of credit cards and what their benefits are below.

How to Choose the Right Credit Card for You

The right credit card for you will depend on your spending habits and how you intend to use it. For instance, if you’re struggling to pay your bills on a monthly basis, getting a credit card may not be the best idea.

However, if you’re in the right place financially, think about how you intend to use your card and what your situation is. Do you just want to build credit? Do you want rewards for spending and can you afford annual fees? If you’re a student, student credit cards may be the best option. Otherwise, think of the other types of cards available to you. This step will help determine what type of card is right for your needs.

After determining what type of card you want to opt for, compare different card options from different issuers. Take a look at the interest rate, fees and rewards involved along with the eligibility requirements. For instance, if you want a cash back credit card, take a look at the rewards and think about how often you’ll benefit from them. Comparing different cards ensures you get the most ideal rates and rewards that suit your spending habits.

Qualifying for Your First Credit Card

Getting your first credit card is a big financial decision, and navigating the process of getting one is just as exciting. To make the process as smooth as possible, it’s important to learn what the requirements are beforehand and the steps to applying.

Getting a Credit Card for the First Time

When you apply for your first card, evaluating your options thoroughly is important to avoid getting saddled with a card you can’t handle. Below is a quick guide to applying for a credit card for the first time.

- Get a list of the basic requirements and prepare what you have. This usually involves being at least 18 years old, having a Social Security number and providing proof of your income.

- Decide on the type of card you want. By now, you should have some idea of what type of card you’d like to apply for, whether it’s a basic credit-building card or a rewards card.

- Compare different credit cards. Once you know what you want to get, search the market for credit cards that meet your needs. This is also a good time to figure out the maximum threshold for interest rates and fees that you can handle.

- Decide on a card and submit the required information. When you’ve narrowed down your list and are ready to apply, visit the nearest bank branch or submit your requirements online through your desired bank’s respective website.

What Credit Card Issuers Look For

Before you can get your first credit card, keep in mind that credit card issuers require certain information that determines whether you’ll get approved. Note that the information provided will be considered for all credit card applications.

Your financial information – This includes your employment status, income and even your bank account information. These are used to figure out the appropriate credit limit for your card.

Your financial information – This includes your employment status, income and even your bank account information. These are used to figure out the appropriate credit limit for your card.- Your personal details – Some personal information you’ll have to submit include your date of birth, Social Security number, citizenship, address and contact details. You may also be asked for your housing situation, such as if you’re renting, are a homeowner or live with others.

Your credit history – This will include any details about any loans you may have. Note that having a limited credit history can affect your chances of credit card approval, as it determines how creditworthy you are.

Your credit history – This will include any details about any loans you may have. Note that having a limited credit history can affect your chances of credit card approval, as it determines how creditworthy you are. Your credit score – If you already have a credit score, whether it comes from loans or paying your bills on time, your card-issuing bank will ask for it. If you don’t have an established credit score yet, expect your credit card options to be limited as this often carries the most weight in approval decisions.

Your credit score – If you already have a credit score, whether it comes from loans or paying your bills on time, your card-issuing bank will ask for it. If you don’t have an established credit score yet, expect your credit card options to be limited as this often carries the most weight in approval decisions.

What to Do if Your Credit Card Application Is Denied

If you’re applying for a credit card for the first time and have limited credit history and no credit score, there is a chance your application may be declined. While this can be disappointing, know that you are free to apply again, but it’s best if you do it after a few months. Learn how to navigate a denied application so you can get approved next time you apply. You may be able to contact the card issuer directly, resolve any issues over the phone and get approved.

- Find out why – If your application is rejected, the Fair Credit Reporting Act legally requires the card-issuer to detail their decision through an adverse action letter. A few reasons you may be denied could be filling out the application incorrectly, having an insufficient income or having a large amount of debt to pay off. Finding out why you were rejected can help you improve your chances the next time you try to apply.

- Wait before reapplying – Avoid reapplying right away. During the application process, banks make inquiries on your credit report, which can ultimately affect your score. The recommended minimum wait time is at least three months, but you can wait as long as six months or more.

- Request for a free credit report – After your application is denied, you have about 60 days to request a free copy of the credit report that the bank used to make a decision. Review it when you receive it to see if you can dispute any errors you see.

- Aim to improve what’s needed – While waiting to reapply, you should work on improving your financial or credit profile. For instance, if you were denied due to having an issue with your credit score, try to build your credit in other ways, such as becoming an authorized user on a friend’s or family member’s credit card, or applying for a credit-builder loan to help you make regular payments. You can look into a secured credit card to help you pay off your bills on time and spend responsibility before moving on to an unsecured card.

Use Your Credit Card Responsibly

A credit card can make dealing with finances more rewarding and convenient, but it can be easy to get carried away. Purchases used via credit can stack up quickly, and before you know it, you may accrue more debt than you can handle. This can have long-lasting damage to your credit score and future finances.

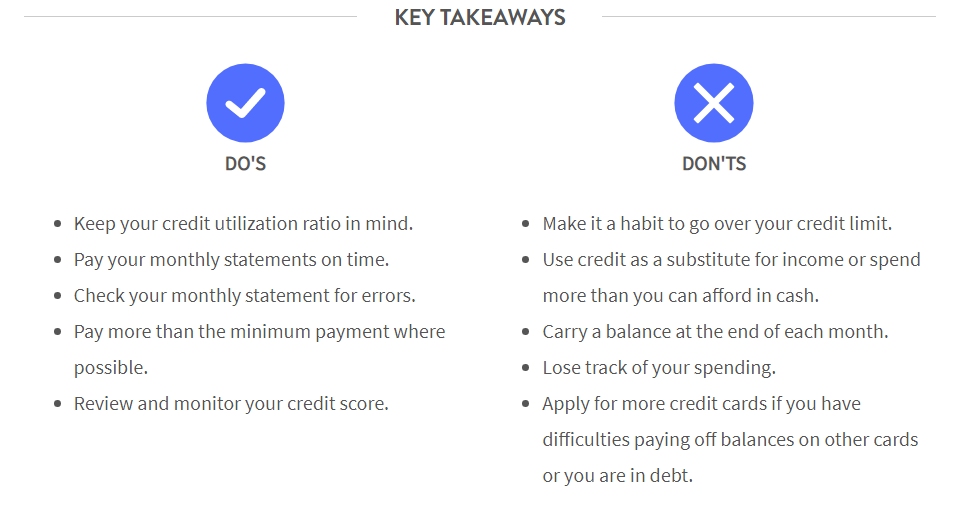

Do’s and Don’ts When Using Your Credit Cards

Viewing credit cards as financial tools and learning how to use them responsibly is the key to avoid getting into significant debt. Below are a few basic do’s and don’ts to keep in mind when you finally have your credit card in hand.

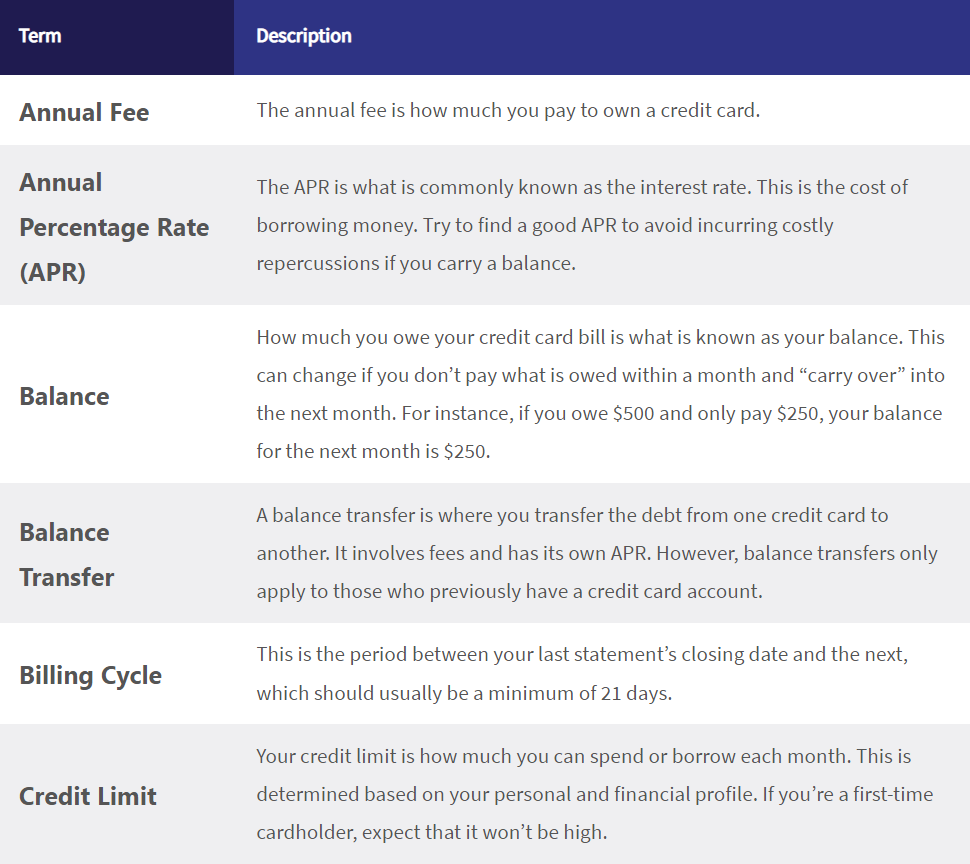

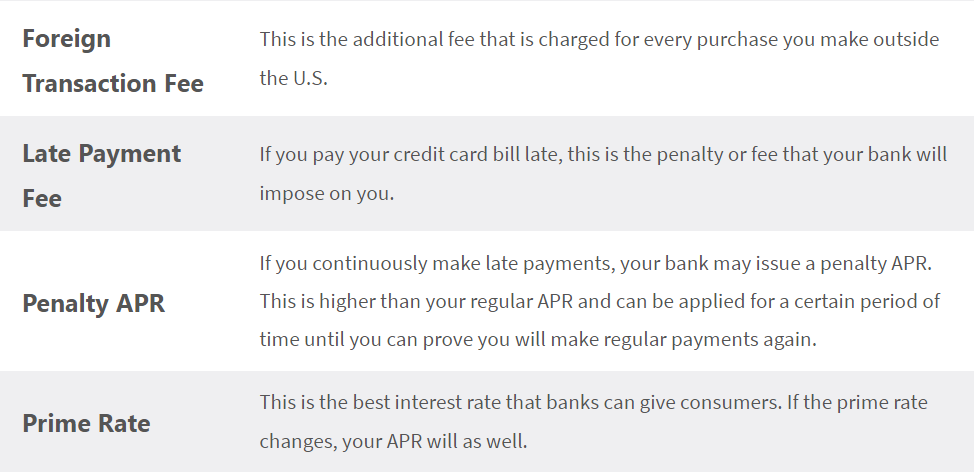

Key Terms to Know Before Applying for a Credit Card

When you apply for a credit card, you may encounter a few terms that can be confusing to understand. To choose the best card for you, make sure to understand the key credit card terms prior to research.

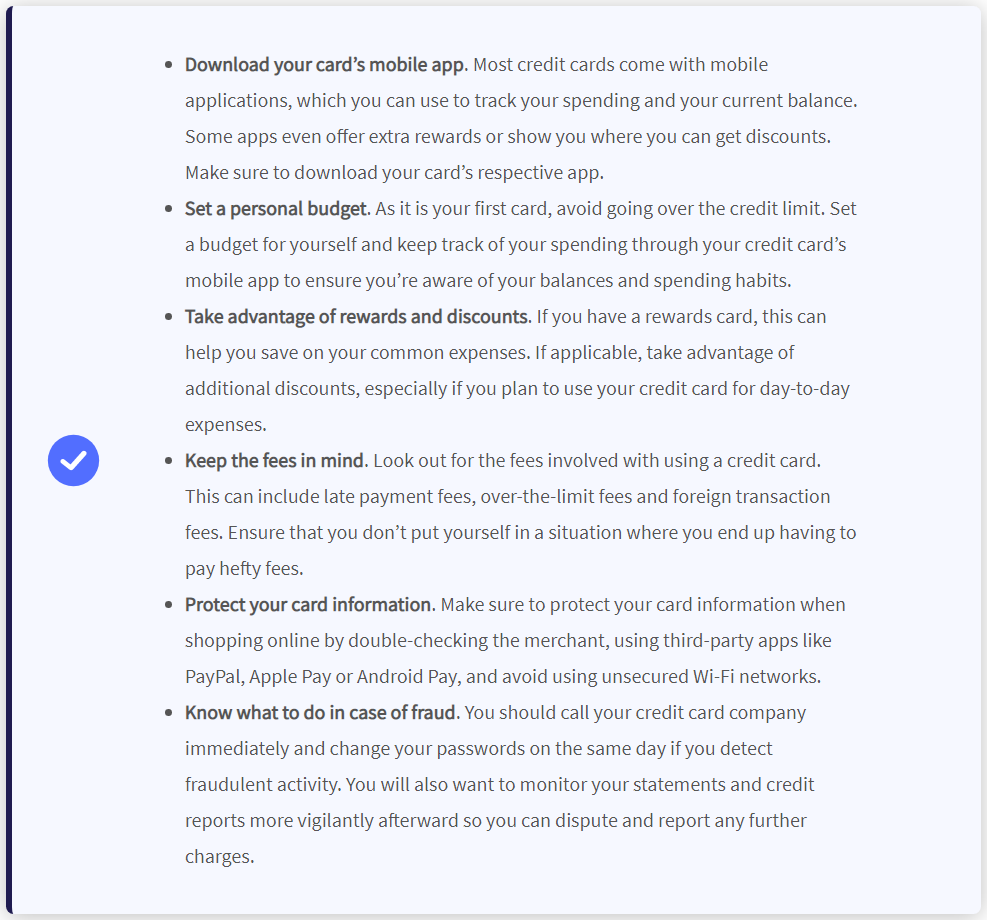

Important Credit Cards Tips You Should Know

Credit cards are a step towards building a better financial future and foundation, but knowing how to use and maintain them is equally important. To maximize the benefits and avoid overspending, keep the following tips in mind.

How to Budget With a Credit Card

Budgeting with your credit card is essential to ensure responsible card use and a good credit score. After all, you don’t want to end up with a mountain of debt after getting your first card. Below are a few tips in order to maintain a budget with your credit card.

- Set an overall limit – You don’t want to end up using most or all of your credit limit, as it’s recommended that you only keep your credit utilization below 30% of your actual limit. Having a limit also ensures that you don’t use your credit card for all your spending.

- Track your spending – Tracking your spending is an essential part of any budget. Fortunately, as most credit cards come with a mobile app or online portal, tracking your expenses has become even easier. This can help you learn your spending habits and decrease unnecessary purchases.

- Avoid carrying a balance – By properly tracking your purchases and staying within your financial means, you can avoid carrying a balance on your credit card.

- Adjust your billing schedule – If you can choose the date of your credit card billing cycle, opt for a date that aligns with your pay period to make your payments easier. This also ensures you pay your bills on time and stay within your spending limits.

- Use your rewards – If your card comes with any offers or rewards for common expenses, make use of them. This way, whatever you save can be put towards any savings, investments or debt.

Expert Insight on Your First Credit Card

Applying for a credit card is an exciting prospect, but is one that needs to be carefully evaluated. MoneyGeek consulted experts within the financial industry for insight on what you need to know about getting your first credit card.

- What is the best advice to give first-time credit card applicants and holders?

- What are some key reasons that indicate that it’s not the right time to get a credit card?

Resources for Getting Your First Credit Card

Learning about how credit cards work is crucial to ensure that you use them right. Below are a few resources to help you learn more about getting your first credit card and ensure you’re on the path toward making the right financial choices to avoid debt.

- Consumer.gov: Learn more about the basics of using credit, what it involves and what to do in this guide by Consumer.gov.

- Consumer Financial Protection Bureau: This worksheet from the CFPB lets you create personal rules to live by when it comes to your credit.

- Federal Student Aid: Geared for college students, this guide by the FSA provides more information on financial literacy and making sound financial decisions regarding a vast number of financial products, such as credit cards.

- Federal Trade Commission: As a first-time credit cardholder it’s important to learn how to settle any credit card debt should it become too large for you to handle. Learn about debt settlement in this guide from the FTC. Using the FTC’s budget sheet can help you get started.

- Junior Achievement: Dedicated to teaching students about workforce readiness and financial literacy through hands-on programs, the JA organization is a great option for students who want to learn more about life after graduation.

- National Endowment for Financial Education: For those who want to receive financial education, NEFE provides programs that can help people take control of their finances regardless of their income level.

- National Foundation for Credit Counseling: The NFCC is a nonprofit network of credit counseling organizations that are dedicated to counseling those who need debt relief. Utilizing the NFCC’s credit card payment calculator can help you determine how much you’d pay in interest and how you can plan to pay off debt.

- Financial Counseling Association of America: The FCAA is a nonprofit organization represented by financial counseling companies. It offers people a range of counseling, such as credit, housing, student loan and bankruptcy. FCAA members also provide assistance and support for debt management and financial education.

- Society for Financial Education & Professional Development: The SFEPD provides financial education and professional development seminars and workshops for college students and for those in the workforce.

To read the full article, click here.