[et_pb_section fb_built=”1″ _builder_version=”4.0.9″][et_pb_row _builder_version=”4.0.9″][et_pb_column type=”4_4″ _builder_version=”4.0.9″][et_pb_text _builder_version=”4.0.9″ hover_enabled=”0″]

Finding the Best Jewelry Insurance

[/et_pb_text][/et_pb_column][/et_pb_row][et_pb_row _builder_version=”4.0.9″][et_pb_column type=”4_4″ _builder_version=”4.0.9″][et_pb_text _builder_version=”4.0.9″]

Got a jewelry box that could make a treasure chest blush? Or maybe you found the Heart of the Ocean necklace from Titanic. No matter what kind of jewelry you’re holding onto, it deserves to be protected, doesn’t it?

But maybe you think it costs too much to insure—it really doesn’t. Or maybe you don’t think it’s worth the hassle—it is, and it’s actually pretty simple.

What Is Jewelry Insurance?

Simply put, jewelry insurance is a policy designed to cover your jewelry (any kind you specify – from rings to Rolexes, it’s all good).

In exchange for the premiums you pay, your insurance carrier will reimburse your financial losses – or even replace the item – in the event of theft, mysterious disappearance, or damage up to its specified value.

Is My Jewelry Covered under Homeowners Insurance?

Yes, but coverage under your homeowners policy is limited to only a small number of causes, like theft, and has a cap of $1,500.

If you want to make sure you’re covered for the full value (should a super-expensive bauble get stolen, for example), you’ll need an additional policy or endorsement.

A more comprehensive coverage option is to schedule personal property coverage. This covers a greater number of risks and will generally cover the full value of higher-priced items that exceed the regular policy’s limit.

The scheduling process involves listing each specific item to be covered and its value – determined by an appraisal.

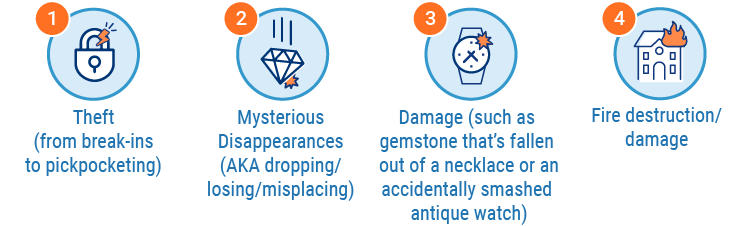

What Exactly Does Jewelry Insurance Cover?

Most everyone’s main concern, when it comes to jewelry, is potential theft – but they’re also worried about losing it. Luckily, jewelry insurance covers the following, for all types of jewelry:

How Do I Insure My Jewelry?

First, you’ll want to contact an insurance agent. They’ll run you through all the ins and outs of the entire ordeal, including:

- Know what jewelry you want covered. Then call up your agent and let ‘em know — they’ll help you get things rollin’.

- Schedule an appraisal. Every local jeweler probably has expertise in appraisals – your agent might even be able to get you hooked up with one. Your insurance company will need to know the exact value of your jewels (based on quality/cut/etc.). This process (usually) isn’t free, but it’s a small price to pay to get to the protection your shiny things need.

- Fill out the important paperwork. Submit the official, verifiable documents from the appraisal to your insurance company.

- Hit “redial” and chat with your agent again. They’ll be able to help you take it from here.

How Much Does Jewelry Insurance Cost?

It depends on the coverage you want, your bling’s total value and location, and a few other factors.

“Increasing the theft limit on your homeowners insurance from $1,500 to $10,000, for example, would only add about $25 to your premium.”

The cost to insure a single piece of jewelry will be around $1-$2 for every $100 in replacement cost. If the jewelry in question would cost around $10,000, then the premium would be around $150, on average.

If you’ve got lots of big items scheduled, though, the cost can add up to thousands or even millions per year, if you’re some kind of Hollywood A-Lister.

Is Jewelry Insurance Worth the Cost?

If all your jewels and jinglies have a value of over $1,500 and you tend to drop, lose or misplace items on a regular basis, then yes, it’s completely worth it.

Also, Martin points out that a lot of jewelry has sentimental value. So, protection could be worth it based on the fact that the item(s) have meaning for you, alone.

If you’re still weighing your decision, it’s best to just ask yourself, “How easily can I afford to replace an item or all the items if something happens to them?” If the answer is “Not easily,” get the insurance.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]