[et_pb_section fb_built=”1″ _builder_version=”4.0.9″][et_pb_row _builder_version=”4.0.9″][et_pb_column type=”4_4″ _builder_version=”4.0.9″][et_pb_text _builder_version=”4.0.9″]

What’s Depreciation Got to Do with Homeowners Insurance?

[/et_pb_text][/et_pb_column][/et_pb_row][et_pb_row _builder_version=”4.0.9″][et_pb_column type=”4_4″ _builder_version=”4.0.9″][et_pb_text _builder_version=”4.0.9″]

Depreciation may seem like an intimidating idea but it’s really just a basic part of everyday life. In fact, you may already know that your four-bedroom, two-bath, brick abode and the majority of its contents (like furniture, TV, and dishwasher) could lose value over time because of things like age and use.

This loss in property value is commonly referred to as depreciation.

Home depreciation is also an important concept within the insurance world. That’s because it directly influences the claim amount paid by the carrier. Remember, depreciation doesn’t just apply to your home but anything with value like cars or boats.

How Do Insurance Companies Calculate Depreciation?

Calculating depreciation all starts with the property’s Replacement Cost Value (RCV) and its estimated life expectancy. The RCV is the current price of repairing or replacing an item with an equal item. As you probably know, life expectancy is the average amount of time the property can be used.

For example, let’s say your new kitchen appliances are destroyed in a small grease fire. You bought the refrigerator, oven, and dishwasher brand new three years ago. All the appliances were working well at the time and in normal condition for their age.

The same kitchen equipment is currently sold in several retail stores for about $3,200 (RCV) new. These three appliances have a life expectancy of 10 years which means they lose 10% of their value each passing year.

In your case, the appliances lost 30% or $960 in value (10% annual depreciation x 3 years of use) at the time of the grease fire.

The example we just gave you is specific to property within your home. Now let’s talk about the structural elements of your home. Parts of your dwelling like the gutters and furnace are also subject to depreciation.

For example, asphalt roof shingles normally last around 20 years and typically depreciate 5% per year. Let’s say your roof is 15 years old at the time of a wind/hail storm. This means the insurance company will subtract 75% of the value (15 years x 5% depreciation per year) of a brand new replacement roof.

How Will Depreciation Determine My Claim Payout?

The first thing that will determine your claim payout is the terms of your policy. Some homeowners coverage is based on an Actual Cash Value (ACV) claims reimbursement schedule. Other homeowners plans are based on a Replacement Cost Value (RCV) schedule. We’re going to review the difference with you.

Of course, depreciation is the second thing that will influence the claims settlement amount you actually receive. Now you may be wondering how ACV, RCV, and depreciation all come together in the claims process? What types of calculations are the insurance companies doing before they mail you a claims check?

Actual Cash Value Example

Let’s assume you have ACV coverage for your residence and personal property kept within the home.

This means the insurance carrier will first determine the Replacement Cost of the item (in other words, how much money it would take to replace the damaged/lost item), then subtract the depreciation amount from the Replacement Cost. The difference between the two amounts is the ACV.

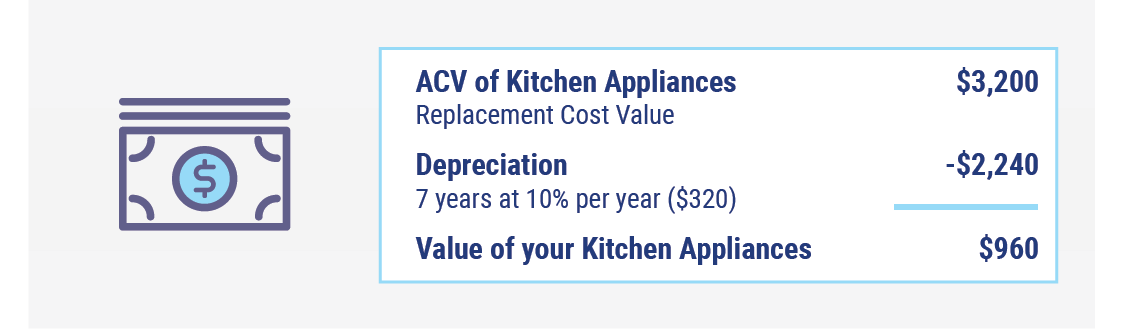

Using the above kitchen appliance scenario, here’s how home insurers calculate RCV if the appliances were destroyed after seven years:

You see here that the insurance company would reimburse you $960 for your destroyed dishwasher, oven, and fridge. That’s because an ACV policy doesn’t promise to give you all the money needed to buy brand new replacements.

Instead, an ACV policy is promising to pay you the depreciated amount of your property. Or, in other words, an ACV policy is insuring your home and property according to what the value is at the time of the loss, not the value at the time you first purchased the house or its contents.

Now if you have a Replacement Cost policy, you should expect to get the full $3,200 for shiny new kitchen gadgets. This means less money out of your own pocket to put your kitchen back together again. It also means quite a bit more in home insurance premiums too.

If you aren’t sure which policy you currently have then we suggest you pull out the policy booklet and take a look. Or give your local, independent insurance agent a call for help understanding if you have an ACV or RCV home insurance policy.

What’s a Recoverable Depreciation Clause?

Sometimes you’ll come across a homeowners policy that includes a recoverable depreciation clause. We imagine you are scratching your head right now and saying, “What the heck does that even mean.” Yep, we thought so.

A recoverable depreciation clause permits policyholders to claim the depreciation of their asset along with the Actual Cash Value. In our kitchen example, you could claim the $2,240 depreciation of the appliances. Of course, anything that sounds that good usually has a catch. This is no different.

Insurance policies that include this clause will expect you to repair or replace covered items within a certain time frame. If you didn’t make a needed repair or complete a certain replacement prior to the date of loss, then your recoverable depreciation could be voided.

(You’ll also need to keep very good records to prove that you did follow the rules and regulations of the clause.)

Recoverable depreciation is a feature that is sometimes not worth it when you factor in the deductible. Think about this: your home policy has a $2,000 deductible. Your kitchen claim will get you $960 ACV payout.

Plus, under your special clause, you can also expect to receive the $2,240 depreciation amount. All of this is payable to you after your $2,000 deductible is met. So you’ll end up with a net positive of $1,200 to replace your appliances. Not bad, but not enough to get brand new appliances free and clear.

Want to Know Three Home Depreciation Tips?

There’s still more to know about depreciation. Take a peek at our three top home depreciation tips below.

- Items max out at 90% depreciation and won’t be depreciated beyond that percentage.

- Quality, workmanship, frequency of use, storage, and upkeep are all factors in determining the lifespan (and ultimately depreciation) of an item. For home materials, more specific things like quality of installation, design, and environmental conditions will also make a difference.

- Specialty items like collectibles, fine jewelry, antiques, firearms, and art can actually appreciate, or increase value, over time. That’s why your independent insurance agent will probably recommend purchasing additional coverage for these types of unique valuables.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]