Adjustable-rate mortgages (ARMs) are home loans with a rate that varies. As interest rates rise and fall in general, rates on adjustable-rate mortgages follow. These can be useful loans for getting into a home, but they are also risky. This article covers the basics of adjustable-rate mortgages.

Key Takeaways

- Adjustable-rate mortgages (ARMs) have an interest rate that can be adjusted with the market.

- The interest rate on these mortgages is typically tied to a market index.

- Lenders typically offer a lower fixed initial rate on these mortgages.

- Caps limit how much the interest rate on an ARM can change.

The Rate

Adjustable-rate mortgages are unique because the interest rate on the mortgage adjusts with interest rates in the marketplace. This is important because mortgage payment amounts are determined (in part) by the interest rate on the loan. As the interest rate rises, the monthly payment rises. Likewise, payments fall as interest rates fall.

The rate on your adjustable-rate mortgage is determined by combining a set ARM margin with a market index. Many adjustable-rate mortgages are tied to the London interbank offered rate (LIBOR), prime rate, cost of funds Index, or another index. The index your mortgage uses is a technicality, but it can affect how your payments change. Ask your lender why they’ve offered you an adjustable-rate mortgage based on a given index.

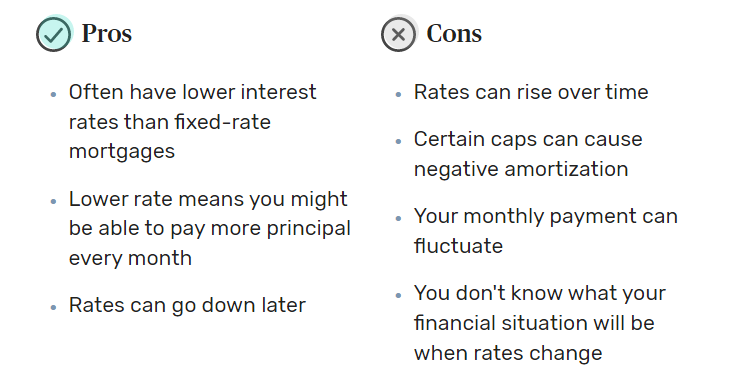

Pros and Cons of ARMs

Adjustable-Rate Mortgage Benefits

The main reason to consider adjustable-rate mortgages is that you may end up with a lower monthly payment. The bank (usually) rewards you with a lower initial rate because you’re taking the risk that interest rates could rise in the future. Contrast the situation with a fixed-rate mortgage, where the bank takes that risk. Consider what happens if rates rise: the bank is stuck lending you money at a below-market rate when you have a fixed-rate mortgage. On the other hand, if rates fall, you can simply refinance and get a better rate.

Pitfalls of Adjustable-Rate Mortgages

Alas, there is no free lunch. While you may benefit from a lower payment, you still have the risk that rates will rise on you. If that happens, your monthly payment can increase dramatically. What was once an affordable payment can become a serious burden when you have an adjustable-rate mortgage. The payment can get so high that you have to default on the debt.

Managing Adjustable-Rate Mortgages

To manage the risks, you’ll want to pick the right type of adjustable-rate mortgage. The best way to manage your risk is to have a loan with restrictions and caps. Caps are limits on how much an adjustable-rate mortgage can actually adjust.

You might have caps on the interest rate applied to your loan, or you might have a cap on the dollar amount of your monthly payment. Finally, your loan may include a guaranteed number of years that must pass before the rate starts adjusting—the first five years, for example. These restrictions remove some of the risks of adjustable-rate mortgages, but they can also create some problems.

Different Kinds of Caps

ARM caps can work in a variety of ways. There are periodic caps and lifetime caps. A periodic cap limits how much your rate can change during a given period, such as a one-year period. Lifetime caps limit how much your ARM rate can change over the entire life of the loan.

Assume you have a periodic cap of 1% per year. If rates rise 3% during that year, your ARM rate will only rise 1% because of the cap. Lifetime caps are similar. If you’ve got a lifetime cap of 5%, the interest rate on your loan will not adjust upward more than 5%.

Keep in mind that interest rate changes in excess of a periodic cap can carry over from year to year. Consider the example above where interest rates rose 3% but your ARM mortgage cap kept your loan rate at a 1% increase. If interest rates are flat the next year, it’s possible that your ARM mortgage rate will rise another 1% anyway because you still “owe” after the previous cap.

ARM Examples

There are a variety of ARM mortgage flavors available. For example, you might find the following:

- 10/1 ARM Mortgage: the rate is fixed for 10 years, then adjusts every year (up to the cap, if there is one)

- 7/1 ARM Mortgage: the rate is fixed for 7 years, then adjusts every year (up to the cap, if there is one)

- 1-Year ARM Mortgage: the rate is fixed for one year then adjusts annually up to any caps

Not All Caps Are Created Equal

Note that caps may differ over the life of your loan. The first adjustment may be up to 5%, while subsequent adjustments may be capped at 1%. If this is the case on an adjustable-rate mortgage you’re considering, be prepared for a wild swing in your monthly payments when the first reset rolls around.

Pitfalls of Caps

While caps and restrictions may protect you, they can cause some problems. For example, your ARM may have a limit on how high the monthly payment will go regardless of movements in interest rates. If rates get so high that you hit the upper (dollar) limit on your payments, you may not be paying off all the interest you owe for a given month. When this happens, you get into negative amortization, meaning your loan balance actually increases each month.

Buyer Beware

The bottom line with adjustable-rate mortgages is that you need to know what you’re getting into. Your lender should explain some worst-case-scenarios so that you aren’t blindsided by payment adjustments. Most borrowers look at these what-ifs and assume that they will be in a better position to absorb payment increases in the future, whether it’s five or 10 years out. This very well may be the case, but things don’t always work out the way we’ve planned.

To read the full article, click here.