5 ways to double your assets through investment

Doubling money is a prospect that few people would turn down, and it isn’t necessarily that difficult to achieve. There are actually various ways to go about making this a reality, depending on your time line and tolerance for risk. You don’t need to buy speculative investments to double your money. A carefully balanced portfolio or even one just filled with super low-risk bonds can get the job done—provided that you are patient and not in a huge rush.

KEY TAKEAWAYS

- There are five key ways to double your money, ranging from a conservative strategy of investing in savings bonds to an aggressive approach involving speculative assets.

- The classic approach of doubling your money by investing in a diversified portfolio of stocks and bonds is probably the one that applies to most investors.

- Investing to double your money can be done safely over several years, but for those who are impatient, there’s more of a risk of losing most or all of their money.

- Be honest about your risk tolerance. Don’t let greed and fear have an adverse impact on your investment decisions, and be extremely wary of get-rich-quick schemes.

- One of the best ways to double your money is to take advantage of retirement and tax-advantaged accounts offered by employers, notably 401(k)s.

Five Ways to Double Your Money

Doubling your money is actually a realistic goal that most investors can strive toward, and it is not as daunting a prospect as it may seem initially for a new investor. There are a few caveats, however:

- Be very honest with yourself (and your investment advisor, if you have one) about your risk tolerance. Finding out that you don’t have the stomach for volatility when the market plunges 20% is the worst possible time to make this discovery and may prove detrimental to your financial well-being.

- Don’t let the two emotions that drive most investors—greed and fear—have an adverse impact on your investment decisions.

- Be extremely wary about get-rich-quick schemes that promise you “guaranteed” sky-high results with minimal risk, because there’s no such thing. Since there are probably many more investment scams out there than there are sure bets, be suspicious whenever you’re promised results that appear too good to be true. Whether it’s your broker, your brother-in-law, or a late-night infomercial, take the time to make sure that someone is not using you to double their money.

Broadly speaking, there are five ways to double your money. The method you choose depends largely on your appetite for risk and your time line for investing. You may also consider adopting a mix of these strategies to achieve your goal of doubling your money.

1. The Classic Way

Investors who have been around for a while will remember the classic Smith Barney commercials from the 1980s in which British actor John Houseman informs viewers in his unmistakable accent that “they make money the old-fashioned way—they earn it.”

When it comes to the most traditional way of doubling your money, that commercial is not too far from the truth. The time-tested way to double your money over a reasonable amount of time is to invest in a solid, balanced portfolio that’s diversified between blue-chip stocks and investment-grade bonds.

The S&P 500 Index—the most widely followed index of blue-chip stocks—returned about 9.8% annually (including dividends) from 1928 to 2020, while investment-grade corporate bonds returned 7.0% annually over this 93-year period.1 Thus, a classic 60/40 portfolio (60% equities, 40% bonds) would have returned about 8.7% annually during this time. Based on the Rule of 72, such a portfolio should double in about 8.3 years and quadruple in approximately 16.5 years.

Note, however, that a significant amount of volatility generally accompanies such sterling results. Investors should brace themselves for occasional sharp drawdowns, such as the 35% plunge in the S&P 500 within a six-week period in the first quarter of 2020 as the coronavirus pandemic erupted worldwide.

In addition, very high returns compared with the historical norm may reduce the potential for future returns. For example, the S&P 500 recovered from its 2020 plunge in record time and powered its way to new record highs by year-end 2020. Although it returned a jaw-dropping total return of 100% from 2019 to 2021, such stellar returns may mean that future returns from the S&P 500 could be significantly lower.

What About Real Estate?

Real estate is another traditional way to build wealth, although it is a far less attractive proposition at times like the present, when housing prices in North America have surged to record levels in many regions. The prospect of rising interest rates also reduces the appeal of real estate investment.

That said, during a real estate boom, the prospect of doubling one’s money proves irresistible to many investors because the huge amount of leverage provided from mortgage financing can really juice up returns. For example, a 20% down payment on an investment property worth $500,000 would require an investor to plunk down $100,000 and get a mortgage for the balance of $400,000. If the property appreciates 20% to $600,000 in the next few years, the investor now has equity worth $200,000 in it, which represents a doubling of the original $100,000 investment.

2. The Contrarian Way

Even the most unadventurous investor knows that there comes a time when you must buy—not because everyone is getting in on a good thing, but because everyone is getting out.

Just as great athletes go through slumps when many fans turn their backs, the stock prices of otherwise great companies occasionally go through slumps, which accelerate as fickle investors bail out. As Baron Rothschild supposedly once said, smart investors “buy when there is blood in the streets, even if the blood is their own.”

Nobody is arguing that you should buy garbage stocks. The point is that there are times when good investments become oversold, which presents a buying opportunity for investors who have done their homework.

Valuation metrics used to gauge whether a stock may be oversold include a company’s price-to-earnings ratio and book value. Both measures have well-established historical norms for the broad markets and for specific industries. When companies slip well below these historical averages for superficial or systemic reasons, smart investors smell an opportunity to double their money.

Being contrarian means that one is going against the prevailing trend. Therefore, it requires a greater degree of risk tolerance and a substantial amount of due diligence and research. As such, a contrarian strategy is best left to very experienced investors and is not recommended for a conservative or inexperienced investor.

3. The Safe Way

Just as the fast lane and the slow lane on the highway will eventually get you to the same place, there are quick and slow ways to double your money. If you prefer to play it safe, bonds can be a less hair-raising journey to the same destination.

Consider zero-coupon bonds, for example. For the uninitiated, zero-coupon bonds may sound intimidating. In reality, they’re simple to understand. Instead of purchasing a bond that rewards you with a regular interest payment, you buy a bond at a discount to its eventual value at maturity.

One hidden benefit is the absence of reinvestment risk. With standard coupon bonds, there are the challenges and risks of reinvesting the interest payments as they’re received. With zero-coupon bonds, there’s only one payoff, and it comes when the bond matures. On the flip side, zero-coupon bonds are very sensitive to changes in interest rates and can lose value as interest rates rise; this is a risk factor to be considered by an investor who does not intend to hold a zero-coupon bond to maturity.

4. The Speculative Way

Although slow and steady might work for some investors, others find themselves falling asleep at the wheel. For folks with a high degree of risk tolerance and some investment capital that they can afford to lose, the fastest way to supersize the nest egg may be the use of aggressive strategies such as options, margin trading, penny stocks, and in recent years, cryptocurrencies. All can super-shrink a nest egg just as quickly.

Stock options, such as simple puts and calls, can be used to speculate on any company’s stock. For many investors, especially those who have their fingers on the pulse of a specific industry, options can turbocharge a portfolio’s performance.

Each stock option potentially represents 100 shares of stock. This means that a company’s price might need to increase only a small percentage for an investor to hit one out of the park. Just be careful and be sure to do your homework before trying it.

For those who don’t want to learn the ins and outs of options but do want to leverage their faith or doubts about a particular stock, there’s the option of buying on margin or selling a stock short. Both of these methods allow investors to essentially borrow money from a brokerage house to buy or sell more shares than they actually have, which in turn raises their potential profits substantially. This method is not for the faint of heart. A margin call can back you into a corner, and short selling can generate infinite losses.

Lastly, extreme bargain hunting can turn pennies into dollars. You can roll the dice on one of the numerous former blue-chip companies that have sunk to less than a dollar. Or, you can sink some money into a company that looks like the next big thing. Penny stocks can double your money in a single trading day. Just keep in mind that the low prices of these stocks reflect the sentiment of most investors.

As Bitcoin has grown in popularity and become more mainstream, other cryptocurrencies have also emerged in recent years as one of the favored ways for speculators to make a quick buck. Although Bitcoin surged 60% in 2021, its performance pales in comparison with that of as many as 10 other cryptocurrencies (with a market capitalization of at least $10 billion) that soared 400% or more in 2021, such as Ethereum, Cardano, Shiba Inu, Dogecoin, Solana, and Terra. (Solana and Terra gained more than 9,000% in 2021 but have seen sharp declines in 2022.)

Unfortunately, the cryptocurrency arena is a fertile hunting ground for scamsters, and there are numerous instances of crypto investors losing a great deal of money through fraud. Would-be cryptocurrency investors should therefore take the utmost care when putting their hard-earned money into any cryptocurrency.

5. The Best Way

Although it’s not nearly as fun as watching your favorite stock on the evening news, the undisputed heavyweight champ is an employer’s matching contribution in a 401(k) or another employer-sponsored retirement plan. It’s not sexy, and it won’t wow the neighbors, but getting an automatic 50 cents for every dollar you save is tough to beat.

Even better is the fact that the money going into your plan comes right off the top of what your employer reports to the Internal Revenue Service (IRS). For most Americans, this means that each dollar invested costs them only 65 to 75 cents.

If you don’t have access to a 401(k) plan, you still can invest in an individual retirement account (IRA), either traditional or Roth. You won’t get a company match, but the tax benefit alone is substantial. A traditional IRA has the same immediate tax benefit as a 401(k). A Roth IRA is taxed in the year when the money is invested, but when it’s withdrawn at retirement, no taxes are due on the principal or the profits.

Either type of IRA is a good deal for the taxpayer. But if you’re young, think about that Roth IRA. Zero taxes on your capital gains? That’s an easy way to get a higher effective return. If your current income is low, the government will even effectively match some portion of your retirement savings. The Retirement Savings Contributions Credit reduces your tax bill by 10% to 50% of your contribution.

Time Horizon and Risk Tolerance

Your investing time horizon is an extremely important determinant of the amount of investment risk that you can handle and is generally dependent on your age and investment objectives. For example, a young professional likely has a long investment horizon, so they can take on a significant amount of risk because time is on their side when it comes to bouncing back from any losses. But what if they’re saving to buy a house within the next year? In that case, their risk tolerance will be low because they cannot afford to lose much capital in the event of a sudden market correction, which would jeopardize their primary investment objective of buying a house.

Likewise, conventional investing strategy suggests that people in or near retirement should have their funds deployed in safe investments like bonds and bank deposits, but in an era of extremely low interest rates, that strategy carries its own risk, mainly of the loss of purchasing power through inflation. In addition, a retired individual in their 60s with a decent pension and no mortgage or other liabilities probably would have a reasonable amount of risk tolerance.

Let’s now turn to the time and risk attributes of an investment itself. An investment that has the potential to double your money in a year or two is undoubtedly more exciting than one that may do so in 20 years. The issue here is that an exciting, high-growth investment will almost certainly be far more volatile than a staid, “Steady Eddy” type of investment. The higher the volatility of an investment, the riskier it is. This increased volatility or risk is the price that an investor pays for the allure of higher returns.

Important: The risk-return tradeoff refers to the fact that there is a strong positive correlation between risk and return. The higher the expected returns from an investment, the greater the risk; the lower the expected returns, the lower the risk.

How Long Does It Take to Double Your Money?

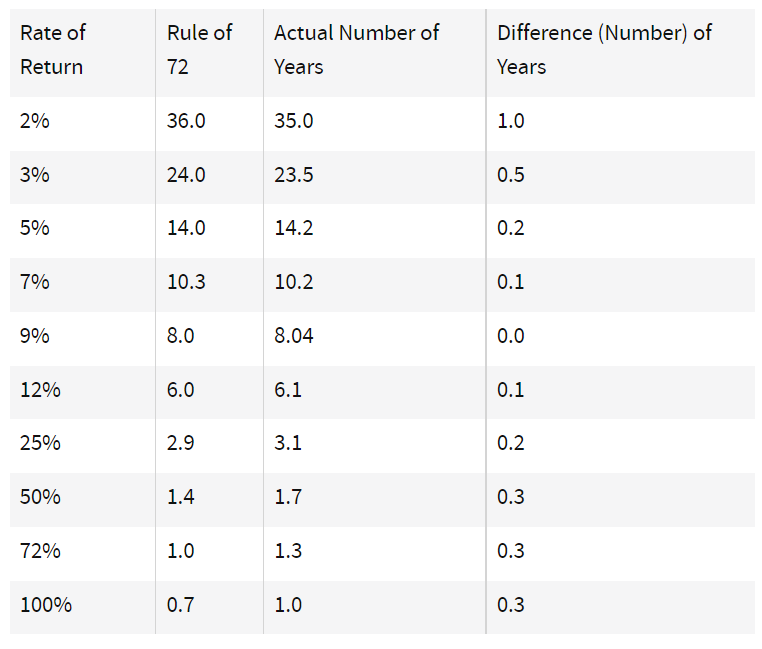

The Rule of 72 is a well-known shortcut for calculating how long it will take for an investment to double if its growth compounds annually. Just divide 72 by your expected annual rate of return. The result is the number of years that it will take to double your money.

When dealing with low rates of return, the Rule of 72 provides a fairly accurate estimate of doubling time. However, that estimate becomes less precise at very high return rates, as can be seen in the chart below, which compares the estimates for “time to double” (in years) generated by the Rule of 72 with the actual number of years that it would take for an investment to double in value.

What’s the single best way to double your money?

It really depends on your risk tolerance, investment time horizon, and personal preferences. A balanced approach that involves investing in a diversified portfolio of stocks and bonds works for most people. However, those with higher risk appetites might prefer dabbling in more speculative stuff like small-cap stocks or cryptocurrencies, while others may prefer to double their money through real estate investments.

Can investors use all five ways in the quest to double their money?

Yes, of course. If your employer matches contributions to your retirement plan, take advantage of that perk. Invest in a diversified portfolio of stocks and bonds and consider being a contrarian when the market plunges lower or rockets higher. If you have the risk appetite and want some sizzle on your steak, allocate a small portion of your portfolio to more aggressive strategies and investments (after doing your research and due diligence, of course). Save on a regular basis to buy a house and keep the down payment in a savings account or other relatively risk-free investment.

Should I invest in cryptocurrencies if I am a conservative investor with very low risk tolerance?

No, you should not invest in cryptocurrencies if you are a conservative investor with very low risk tolerance. Cryptocurrencies are very speculative investments, and although many of them had huge returns in 2021, their tremendous volatility makes them unsuitable for conservative investors.

To read the full article, click here.